Latest Content > The Case Against Mortgage-backed Securities in a World of Residential Tokenized Home Equity Investments

The Case Against Mortgage-backed Securities in a World of Residential Tokenized Home Equity Investments

In the ever-evolving landscape of finance and investment, innovation is key. Traditional financial instruments, such as Mortgage-backed securities (MBS), have long been the bedrock of the real estate market. However, in a world driven by technological advancements and financial creativity, it's time to question whether MBS still hold their relevance. Enter residential tokenized home equity investments, a modern alternative that offers unique advantages and challenges the conventional wisdom of MBS!

Imagine for a moment the unnecessary and complicated infrastructure that has been built in and around Mortgage-backed securities.

- Real estate buyers borrow from financial institutions.

- Financial institutions sell mortgages to MBS entities.

- MBS entities form mortgage pools and issue Mortgage-backed securities.

- Individuals and institutions invest in MBS pools.

All this complex infrastructure for banks to further profit from mortgages. Where the only true beneficiaries are the banks and financial intermediaries… Banks make money on mortgages through a combination of origination fees, interest rate spreads, and fees generated from servicing the loans, and more.

Here are the range of tactics banks use to make money off of mortgages:

- Origination Fees:

- Banks often act as intermediaries between borrowers and the MBS market. They originate mortgages by lending money to homebuyers or homeowners looking to refinance.

- When a bank originates a mortgage, it can charge borrowers various fees, including application fees, loan processing fees, and underwriting fees.

- Securitization:

- Banks bundle individual mortgages together into pools, which serve as the underlying assets for MBS. These pools are then sold to investors in the secondary market.

- The process of creating MBS involves securitization, where banks package the loans, create securities, and issue them to investors.

- Interest Rate Spreads:

- Banks make money from the interest rate spreads between the loans they originate and the MBS they sell in the secondary market.

- For example, a bank may originate a mortgage at a fixed interest rate of 4% and then sell it as part of an MBS with a weighted average interest rate of 3.5%. The bank earns the difference (0.5%) as profit.

- Servicing Fees:

- Banks often retain the responsibility for servicing the loans within an MBS pool. This servicing includes collecting monthly payments from borrowers, managing escrow accounts, and handling delinquencies or defaults.

- Banks also charge borrowers servicing fees, which are typically a percentage of the outstanding loan balance.

- Gain on Sale:

- When banks sell MBS in the secondary market, they may receive a premium above the face value of the underlying loans. This gain on sale represents an additional source of revenue.

- Conversely, if the MBS is sold at a discount, banks may incur a loss.

- Mortgage-Related Investments Hedge and Risk Management:

- Banks may also invest in MBS as part of their own portfolio. This allows them to earn interest income from the MBS while potentially benefiting from capital gains if the securities appreciate in value. Also, Banks use MBS as tools for managing risk. For example, they may purchase MBS to hedge against interest rate fluctuations or to diversify their investment portfolio. These practices contributed to the 2008 financial crisis. Think of it as the fox watching the hen house!

- Fees from Loan Modifications and Refinancing:

- In cases where borrowers within an MBS pool request loan modifications or refinance their mortgages, banks often charge fees for these services.

- Regulatory Benefits:

- Banks even leverage regulatory capital relief by securitizing mortgages. This process reduces the capital requirements associated with holding the loans on their balance sheets, freeing up capital for other activities. As per above, often reinvesting in these same Mortgage-backed securities. By deploying an accounting regulatory sleight of hand they remove debt off their balance sheet and add an MBS as an investment.

Here are the top 5 banks that hold mortgaged backed securities as investments on their balance sheets (Source: American Banker 20 banks and thrifts with the largest Mortgage-backed securities portfolios, by Courtney Hoff, November 22, 2022):

- J.P. Morgan: $3,841,314,000

- Bank of America: $3,111,606,000

- Citi: $2,380,904,000

- Wells Fargo: $1,881,142,000

- Morgan Stanley: $1,173,776,000

It is also important to note that the US Federal Reserve is also one of the largest holders of mortgage backed securities. The Fed currently holds about $2.6 trillion of MBS as part of its roughly $8 trillion securities portfolio (Source: Reuters - Fed needs Mortgage-backed securities exit plan 'earlier than later,' George says, by Howard Schneider, January 23, 2023).

These tactics offer no real tangible benefit to the homeowner and essentially banks are making additional revenue off the homeowner’s debt. Certainly, investors would be better served with direct and transparent access to residential property assets such as direct tokenized home equity investments.

MBS: A Historical Perspective

Mortgage-backed securities emerged in the latter half of the 20th century as a means to provide liquidity to the housing market. These securities pool together thousands of individual mortgages, transforming them into tradable financial assets.

However, history has shown us that MBS are not without their flaws. The financial crisis of 2008 served as a harsh reminder of the serious risks associated with MBS, as their complex structures and opaque valuations contributed to the global economic downturn. This painful experience highlighted the need for alternatives that reduce systemic risks while maintaining investment opportunities within the real estate sector.

Residential Tokenized Home Equity Investments: A Paradigm Shift

Residential tokenized home equity investments represent a compelling alternative to MBS. These investments utilize blockchain technology to tokenize ownership stakes in individual properties, allowing investors to directly participate in the real estate market and bypass financial intermediaries.

Here's why this innovative approach is gaining momentum:

Transparency: Blockchain technology ensures transparency at every level. Every transaction is recorded on an immutable ledger, reducing the risk of fraud and manipulation. Investors can confidently track their investments in real-time, unlike the opacity of MBS.

Liquidity: Tokenized assets are highly divisible and can be traded 24/7, offering greater liquidity compared to traditional real estate investments. This accessibility allows a wider range of investors to participate in the market.

Reduced Intermediaries: MBS typically involve multiple intermediaries, each taking a slice of the pie. With tokenized home equity, the need for intermediaries is greatly reduced, potentially lowering overall transaction costs.

Global Accessibility: Tokenized investments are not limited by geographical boundaries. Investors from around the world can easily access and invest in properties they find promising, broadening the pool of potential investors. Vesta Equity currently has over $16 millionUS in tokenized home equity investments available for purchase. Just scraping the surface of the United States real estate market which sits at just over $3.6 trillion US. The global market is estimated to be as large as $270 trillion US. That’s 3X the size of the global stock markets combined.

Fractional Ownership: Tokenization allows for fractional ownership of properties, enabling investors to diversify their real estate portfolios with smaller capital outlays. This democratizes real estate investment and opens doors to a wider range of investors.

Risk Mitigation: Tokenized home equity investments can offer built-in risk mitigation mechanisms through smart contracts.

Alignment of Interests: Tokenization aligns the interests of property owners and investors more closely. Owners benefit directly from property appreciation and additional yield, fostering a stronger sense of stewardship.

The Path Forward

While residential tokenized home equity investments offer compelling advantages over MBS, it's important to acknowledge that they are still relatively new and evolving. Regulatory considerations, standardization, and market maturity are areas you need to evaluate. Ensure that who you are dealing with is regulatory compliant and they are not using the blockchain, DAOs, or other exotic and half-baked ideas to justify not being compliant. See our recent blog post Is a Tokenized Real Estate Asset Really a Security? to get a sense of what it means to be compliant. Vesta Equity uses blockchain technology, but from launch we have been committed to best practice regulatory compliance.

The fundamental shift in real estate investments made possible by tokenization cannot be ignored! Direct ownership, eliminated intermediaries, and the potential for global diversification make residential tokenized home equity investments a powerful alternative to MBS and with time should replace them.

In a world that demands innovation and transparency, it's time to rethink the traditional approach to real estate investing. Keep your hard earned money where it belongs! In your pocket and investment portfolio and not on some bank’s income statement and balance sheet.

Investment Properties

Vesta Equity offers tokenized home equity investments through its marketplace at https://app.vestaequity.net/marketplace

Sign up to get alerts about new posts

What’s New

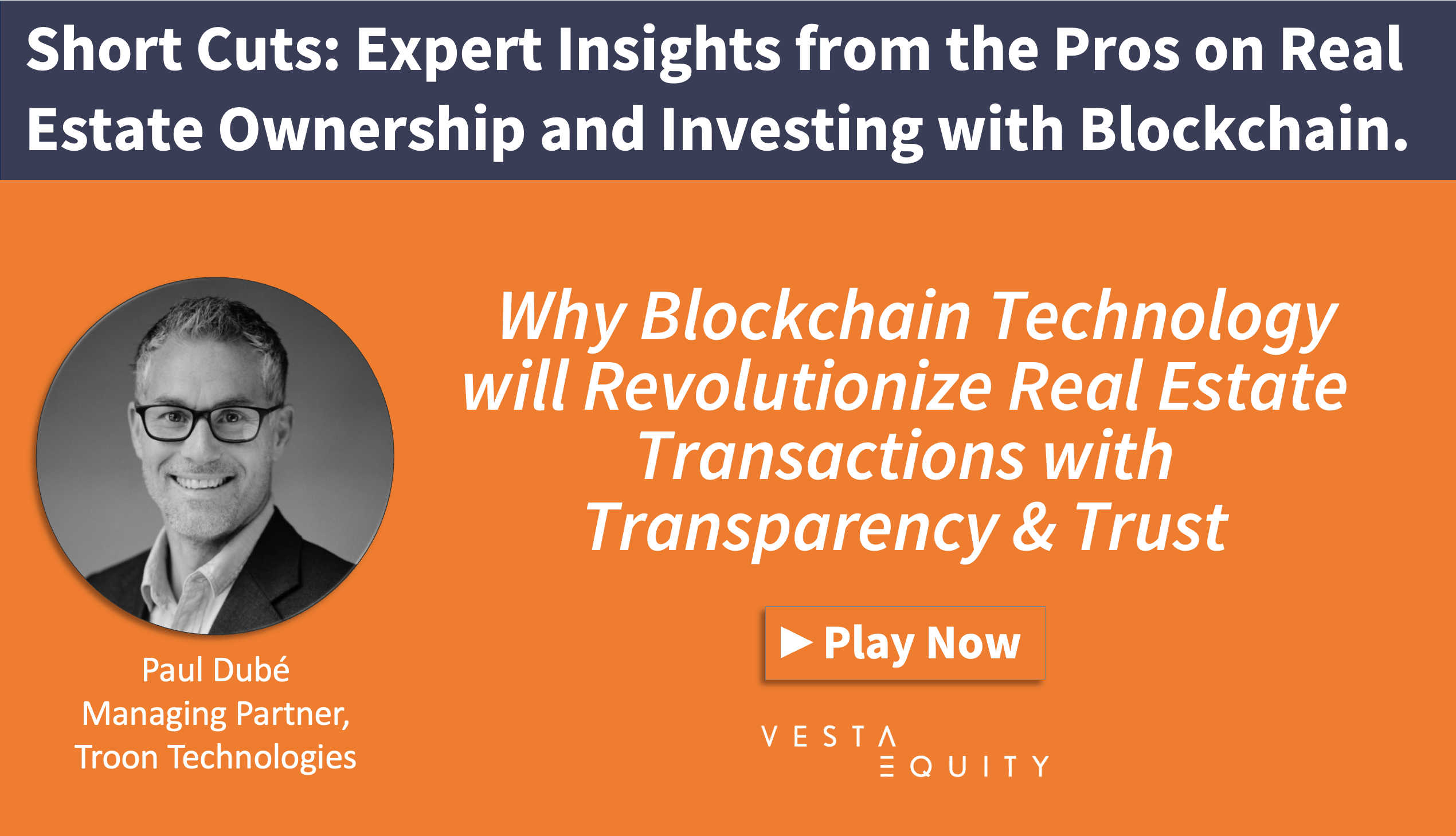

Short Cuts: Expert Insights from the Pros on Real Estate Ownership and Investing with Blockchain

Within Blockchain, numerous fundamental principles are in place to ensure transparency and combat fraud. They commence with the transactions themselves, which are both verifiable and permanent, taking place between two parties within a decentralized network.

Watch Video

Watch Video

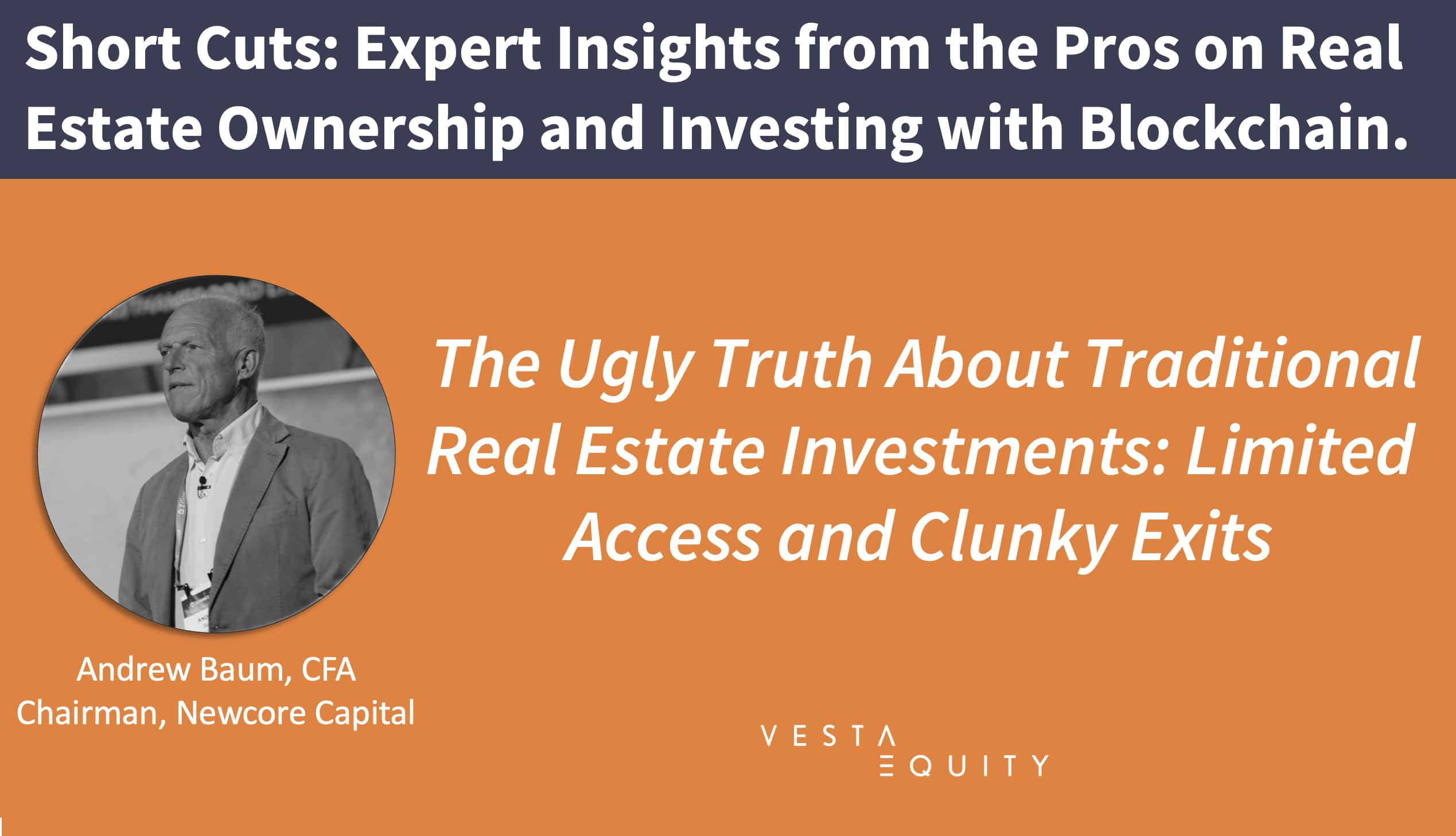

Short Cuts: Expert Insights from the Pros on Real Estate Ownership and Investing with Blockchain

The ugly truth about traditional real estate investments: limited access and clunky exits with Andrew Baum CFA, Chairman of Newcore Capital.

Watch Video